![]()

Stocks rallied across the board; the Dow Jones and the Russell 2000 each rose more than 2 percent.

National Association of Home Builders Housing Market Index:

May (Monday)

Home builder sentiment improved modestly after falling sharply in April. Despite the improvement, the index remained in contractionary territory.

- Expected/prior month sentiment: 34/34

- Actual month sentiment: 37

FOMC Meeting Minutes:

April (Wednesday)

Minutes from the April FOMC meeting suggested a divided central bank. In the post-meeting statement, some members advocated removing language that indicated an easing bias, while others successfully pushed to keep it.

Housing Starts and Building Permits:

April (Thursday)

These two measures of new home construction were mixed in April. Housing starts fell after surging in March, while building permits rebounded following a steep decline the previous month.

- Expected housing starts/prior housing starts: –5.3%/+12.0%

- Actual housing starts: –2.8%

- Expected building permits/prior building permits: 2.5%/–11.5%

- Actual building permits: +5.8%

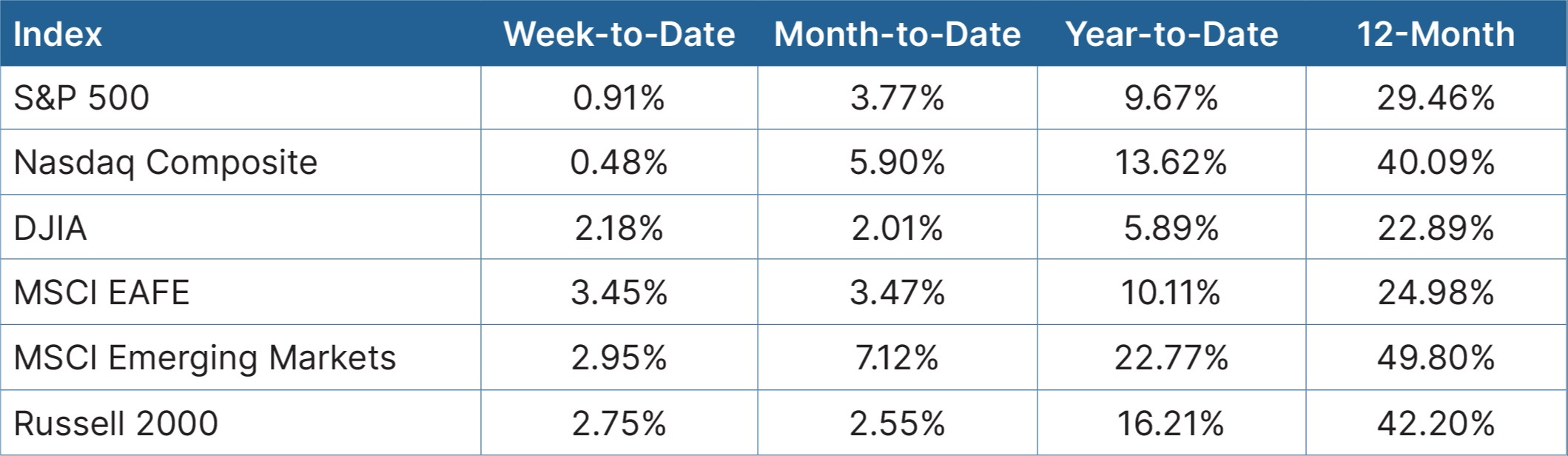

Equity

U.S. markets were higher, but leadership shifted. The Dow Jones and Russell 2000 each rose more than 2 percent, and the Nasdaq Composite and S&P 500 were each up nearly 1 percent. The catalyst was an 8 percent drop in oil prices because of favorable headlines about a potential deal to end the Middle East war. Health care, utilities, and real estate each rose more than 3 percent. Communication services and consumer staples lagged. International equities also rallied; developed markets rose more than 3 percent.

Source: Bloomberg, as of May 22, 2026

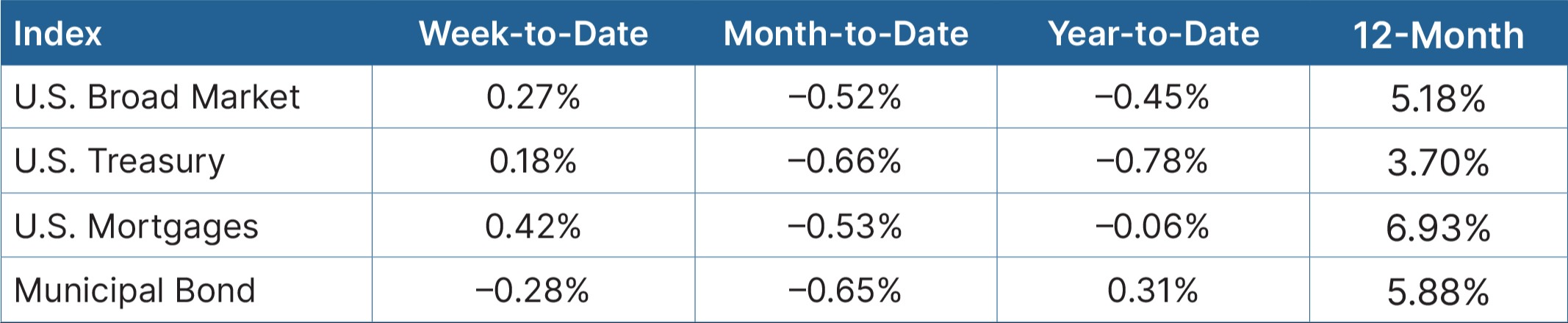

Fixed Income

Fixed income markets were mostly higher. Continued commentary regarding a potential deal to end the war in the Middle East calmed markets. The yield on the 10-year Treasury halted its steep rise, closing at 4.56 percent. This closing yield was down 4 basis points (bps) compared with the previous week. High-yield bonds also moved higher, while the municipal market was flat.

Source: Bloomberg, as of May 22, 2026

Looking Ahead

Consumers will be the focus of economic reports this week. The Conference Board Consumer Confidence Index and personal income and spending data will give investors insight into how consumers are navigating higher energy prices.

- The week kicks off on Tuesday with the Conference Board Consumer Confidence Index for May. It’s expected that confidence will fall after improving modestly in April.

- On Wednesday, we’ll see a report on personal income and spending for April. Both are expected to increase, with personal income rebounding after falling in March.

- Earnings reports continue; highlights include Costco and Dell.